With national dwelling values falling for the third consecutive month, selling conditions across Australia’s unit markets have continued to weaken.

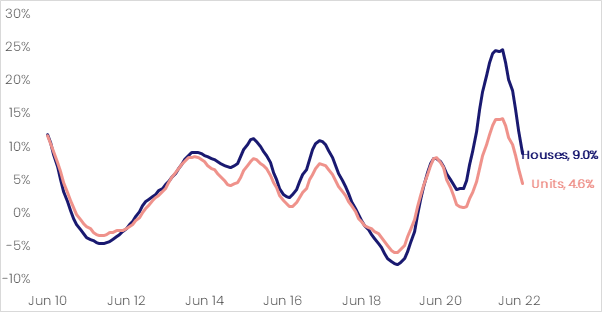

Falling a further -0.9% over the month, and -1.4% over the three months to July, national unit values are now -0.2% lower over the year to date. While national houses have recorded deeper monthly (-1.4%) and quarterly (-2.2%) declines, stronger growth over the first four months of the year means that house values are still 1.2% higher than they were at the beginning of this year. As we move further into the downwards phase of the cycle, the annual performance gap between national houses (9.0%) and units (4.6%) has continued to narrow. Annual house growth has fallen below double digits for the first time since April 2021 (9.3%).

CoreLogic Economist Kaytlin Ezzy says the impacts of consecutive rate hikes are now becoming more wide spread, with the pace of growth easing or falling into negative territory across most market segments.

“Units are relatively more affordable and attract strong investor activity, meaning value changes across the medium to high density sector are proving to be less volatile than the house segment,” Ms Ezzy said.

“However, market factors including increased interest rates, lower consumer sentiment and higher cost of living, mean selling conditions for units have also shifted in favour of buyers.”

The median days on market over the three months to July to the median days on market over the three months to April for Australian unit markets. With the exceptions of South Australia and the Northern Territory, each unit market saw the average selling time increase, as vendors take longer to negotiate a sale.

Compared to the three months to April, units across Hobart and regional Tasmania are now taking approximately three times as long to sell, while nationally, the median time on market has increased by six days. Vendors are also having to offer larger discounts in order to secure a sale, with median vendor discounting nationally increasing from 2.9% over the three months to December to 3.8% over the three months to July.

Rolling annual growth rate, National houses and units

Following the national trend, unit values across the combined capitals decreased for the third consecutive month, down -1.0%, taking capital city unit values -1.8% lower over the three months to July. Coupled with the weaker monthly increases recorded over the first quarter of the year, these declines have seen the annual change in values weaken from 12.7% over the year to January, to just 2.5% over the 12 months to July. Over the same period, annual growth in regional unit values has decreased from 23.7% to 16.1%.

“Across the individual capital city and rest of state unit markets, Hobart and Regional Tasmania recorded the largest decline in values over July, down -2.5% and -2.1% respectively. The sharp deceleration in value growth was likely caused by an increase in newly advertised unit listing across Tasmania in July. While still well below the previous five-year average, this increase saw total advertised unit supply across Hobart rise 51.0% above the levels recorded in July 2021,” Ms Ezzy said.

Unit values across Sydney (-1.5%) fell for the sixth consecutive month, taking values approximately $35,000 lower over the year to date, while unit values across Melbourne fell -1.2% in July and -2.1% over the quarter.

“With consecutive rate hikes and high total listing supply, unit values across Sydney and Melbourne are now just 0.3% and 0.5% above the levels recorded this time last year,” Ms Ezzy said. “Looking at CoreLogic’s daily index, it’s likely Sydney and Melbourne’s annual trend will fall into negative when the August results are reported.”

Regional NSW units decline by -0.4% over the month, taking values back to the levels seen in April, while Regional QLD (-0.3%) and Canberra (-0.2%) recorded the first monthly fall in unit values since August 2020 and April 2020 respectively.

Unit rental values

Growth in rental values continues to surge across Australia’s unit markets, with national rents rising 1.3% in July. This month’s result took national unit rents 3.7% higher over the three months to July and saw the 12 months to July (10.7%) overtake the year to June (10.0%) as the highest annual rental rise on record. This month also marks the third consecutive month where units have outperformed houses in monthly, quarterly and annual growth, across both the combined capital and combined regional markets, as well as at the national level.

“A number of factors are driving demand for unit rentals including unit’s relative affordability. At approximately $493 per week, the average unit rental is still nearly $60 a week cheaper than the average rental value for a house ($552). While national units (10.7%) recorded larger annual percentage rises in rents compared to houses (9.5%), in dollar terms both markets saw weekly rents rise by approximately $48.”

A similar growth trend was seen across the individual capital cities, with each capital recording stronger monthly rental increases across the medium to high density segment compared to the lower density sector. Perth was the one exception, with both house and unit rents rising 0.8% over the month.

Brisbane recorded the strongest increase in unit rents, rising 4.4% over the three months to July, followed by Sydney (4.1%) and Melbourne (3.9%). Adelaide and Darwin both recorded a quarterly increase in rent of 3.8%, while Hobart and Perth saw rents rise 2.2% over the same period. Previously Australia’s most expensive unit rental capital, Canberra recorded the smallest quarterly increase in rents, up just 1.8% over the three months to July. Stronger growth across Sydney, saw its median rental value ($579 per week) rise above Canberra’s median ($578 per week) to become Australia's most expensive capital to rent a unit in.

Outlook for the unit market

The outlook for Australia’s unit market over the short to median term remains pessimistic, with interest rates expected to rise throughout the second half of the year and into 2023, and a surge in fresh listings likely to add further downward pressure on values as we approach the spring selling season.

While strong rental growth and the lowest unemployment rate in nearly 50 years should help the broader housing market by bolstering investor demand and minimising distressed sales, it’s likely dwelling values will continue to decline as interest rates rise. Despite unit values being historically less volatile than house values, thanks in part to their relative affordability, it’s likely unit values will continue to decline as we move further into the downwards phase of the housing cycle.

Download a copy of the Unit Market Update

Meet Kaytlin Ezzy

Economist

Kaytlin Ezzy is an Economist at CoreLogic, Australia’s leading property data, information, analytics and services provider.

Full profile