While inflation has implications for housing demand, housing itself influences inflation. By understanding how inflation and housing fit together, the market outlook for the year ahead becomes a little clearer.

ABS figures showed the highest annual rate of inflation in June 2022 in almost 32 years. As we head into the new financial year, annual inflation is expected to peak at over 7%, according to the Treasury and the RBA. This means household budgets will be tighter, savings will be reduced and housing demand will likely be lower.

While inflation has implications for housing demand, housing itself influences inflation. By understanding how inflation and housing fit together, the market outlook for the year ahead becomes a little clearer.

How does the housing market impact inflation?

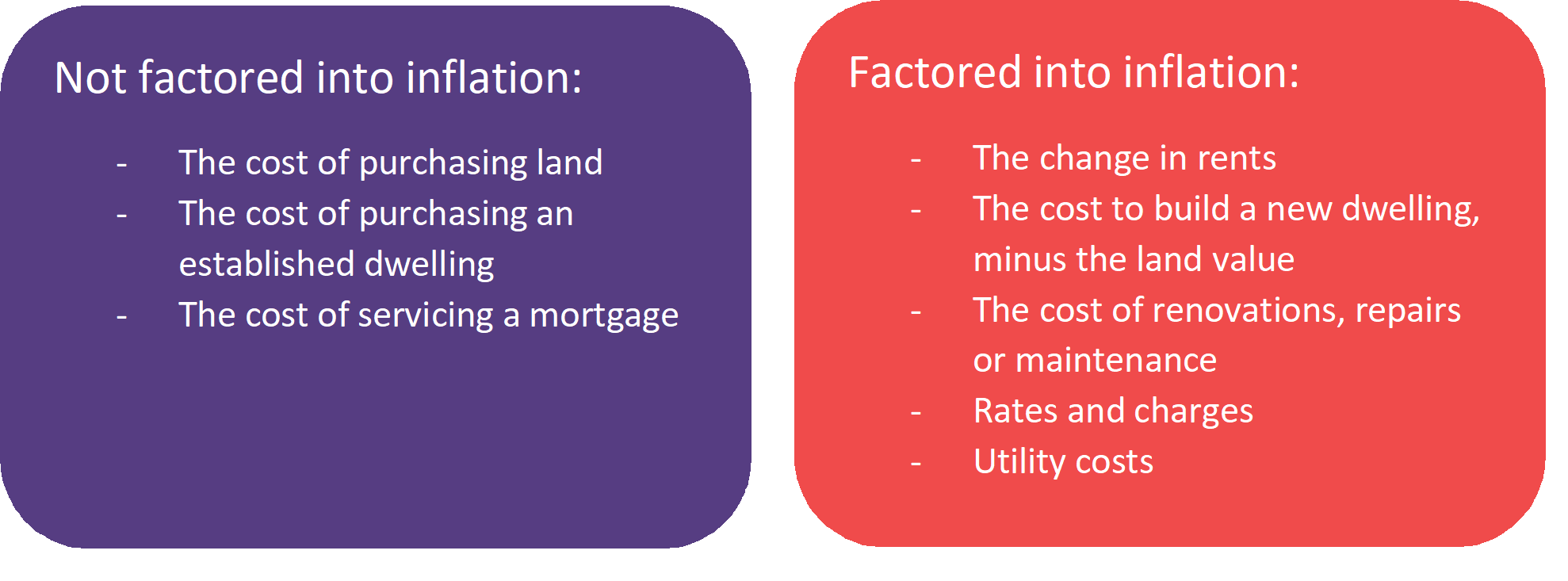

A good place to start is looking at how housing is factored into inflation (see figure 1). Inflation measures the change in the Consumer Price Index (CPI), which tracks the cost of a basket of goods and services consumed by households, specifically bought from other sectors; governments and businesses.

Because established dwellings are traded within the household sector, the change in established dwelling prices over time is not factored into inflation. Land purchases are also not included, as land is considered an asset, not a consumption good.

Mortgage interest costs were excluded from inflation from 1998, in part, because the RBA started setting interest rates in the early 90’s to target inflation. Continuing to measure interest costs made it difficult to understand the impact of monetary policy on genuine cost pressures in the economy.

The cost of new dwellings purchased by owner-occupier households (minus land value) is included in inflation calculations, as well as changes in rent values. Other property-related expenses, such as rates and charges, property repairs, maintenance and renovations, are also factored in.

Figure 1. How is housing factored into inflation?

The housing component of the consumer price index is given the biggest weight of goods and services in the CPI (around 23%, 8.7% for new dwellings, and 6.2% for rents). This reflects the relatively large expenditure households put toward housing costs. As a result, inflation is heavily influenced by changes in rents, new dwelling prices and utility costs. The annual change in the total housing component of the CPI was 9.0% in June 2022. This was the second-largest increase of the CPI components, behind a 13% surge in transport costs.

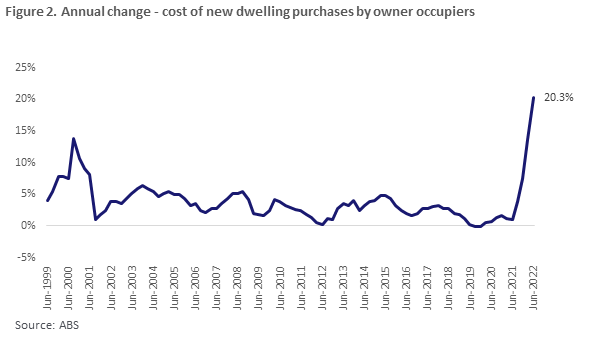

Figure 2 shows the rolling annual inflation in the cost of new dwelling construction within the housing category. In the June 2022 quarter, the annual increase in new dwelling costs for households was 20.3% (a series high). This is well above a series average of 3.9%, highlighting the extreme conditions in the housing construction sector.

Building material supplies have been constrained by supply chain disruptions, while the various construction incentives introduced through the pandemic (such as HomeBuilder, and the ‘new homes’ edition of the first home loan deposit scheme) caused a sudden surge in demand. Though construction pipelines and costs are still inflated, the expiry of these government grants has further added to inflation in this category, with grants and subsidies being factored into CPI.

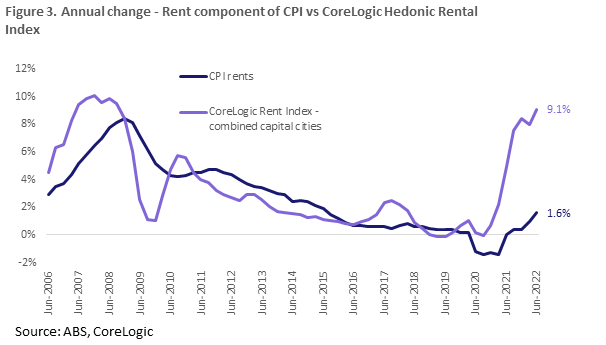

June also saw a 1.6% annual increase in the value of rents. Figure 3 compares the rent component of CPI to the annual change in CoreLogic’s hedonic rental value index.

There is currently a large discrepancy between the CPI measure of rents, and CoreLogic’s rent value index. This is because they measure two different things. CPI rents are measured from a sample of rental properties across private and government housing, to ascertain changes in rents actually paid. The CoreLogic series uses a hedonic regression model across all private dwellings to understand changes in rental valuations.

CoreLogic’s model typically leads trends in rents paid, because it is estimating value based on listings information. This is important, because it can inform future movements in a heavily weighted component of inflation. If CoreLogic’s rent valuations are higher, this indicates households will be facing higher rents actually paid when they go to renew their lease. The fact that annual growth in CoreLogic rental values has shown no signs of slowing, suggests the rent component in inflation could also see further upward pressure in the coming quarters.

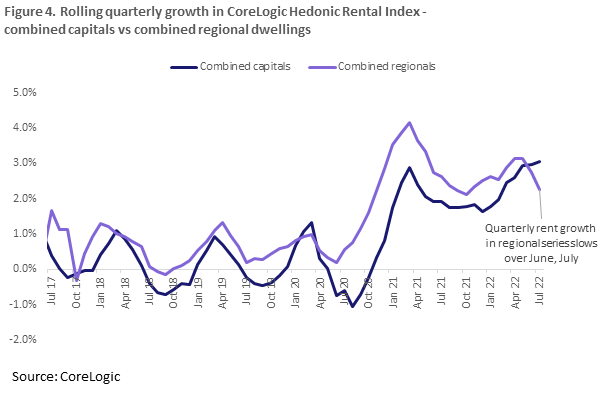

The only early indications of a softening in rental growth may be in the combined regional Australian dwelling series, where rolling quarterly growth in CoreLogic rent valuations softened through June and July (figure 4). It’s early days, but this could indicate rental growth moving through a peak, and a (very) early sign that inflationary conditions could ease as a result.

As overseas migration returns as Australia relaxes travel restrictions, it may take longer for capital city rent growth to slow. This is because many overseas visitors and migrants have housing demand skewed to renting in the capital cities.

Over the past two years, these trends in new builds and rents have contributed to higher inflation. But in turn, the high inflationary environment can impact the housing market in several ways.

How does inflation impact the housing market?

Inflation impacts housing markets both directly and indirectly. But whether these impacts are ‘good’ or ‘bad’ depend on what is driving inflation, as well as what else is going on in the economy at the time.

For example, a direct impact of inflation is that it can erode the value of debt, which is good for mortgage holders. As the economy heats up, wages may rise, but mortgage principals are fixed, meaning mortgage repayments can become relatively low. This was one feature of the high inflationary period of the 1980s; interest rates soared, but inflation and wages growth were also high.

For mortgage holders in 2022, income growth has been more elusive. The wage price index reported by the ABS was up 2.4% in the year to March, below the series average growth of 3.1%, but is climbing. Additionally, national accounts data from the ABS showed a pickup in household income growth from 2021, and RBA monetary policy statements have indicated wages growth is on the way up. But until wages growth picks up substantially, households have to deal with high debt levels and a rising cost of living.

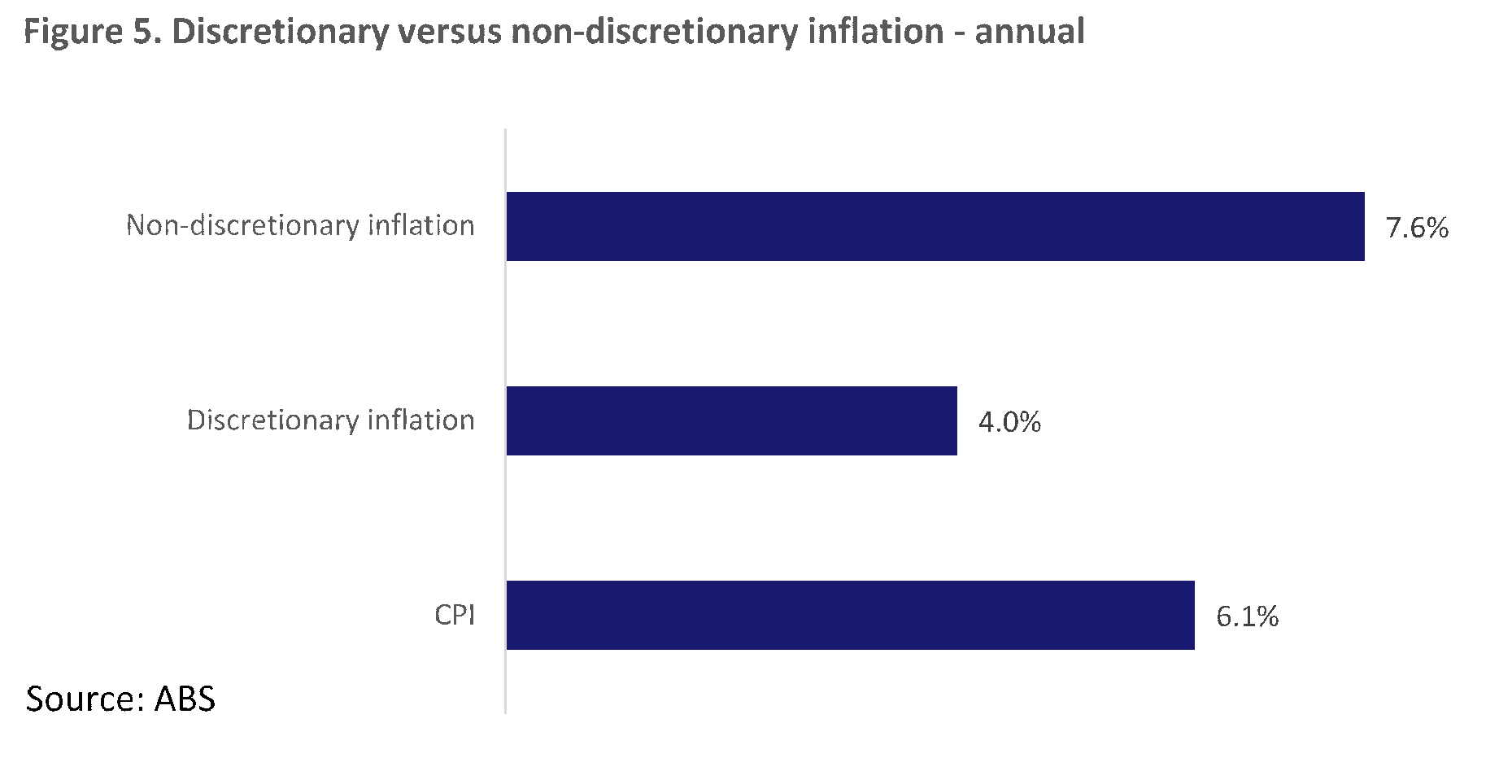

Another key feature of inflation in 2022 is that price rises have been particularly steep in areas where it is hard to cut back on spending. This category of spending, known as ‘non-discretionary’ items, include things like fuel, housing and food. The ABS reported annual inflation in non-discretionary spending was almost twice that of discretionary spending in June 2022 (see Figure 5).

The implication is that mortgage holders are likely to feel more of a pinch in their household budgets, with rising rates adding significantly to mortgage costs at high debt levels, while households may find it difficult to fund these costs by cutting back on things like fuel and food. Instead, discretionary spending is likely to shrink more quickly over the coming months.

The implication is that mortgage holders are likely to feel more of a pinch in their household budgets, with rising rates adding significantly to mortgage costs at high debt levels, while households may find it difficult to fund these costs by cutting back on things like fuel and food. Instead, discretionary spending is likely to shrink more quickly over the coming months.

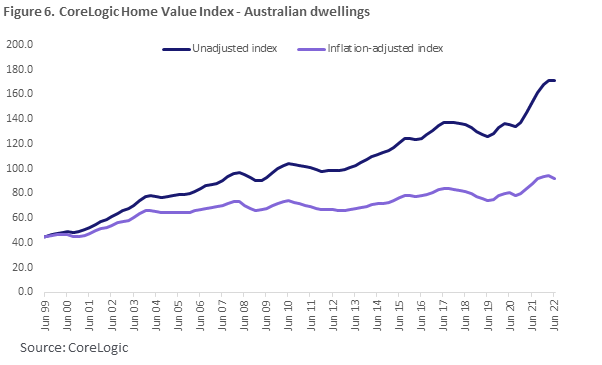

Another direct impact of inflation is that it erodes the real value of housing. Real growth in housing values is calculated using quarterly growth in the CoreLogic Home Value Index, minus quarterly inflation. Figure 6 shows the nominal home value index, alongside the real changes in home values over time. For the June quarter of 2022, the real change in Australian home values was -1.9%, against a nominal decline of -0.2%.

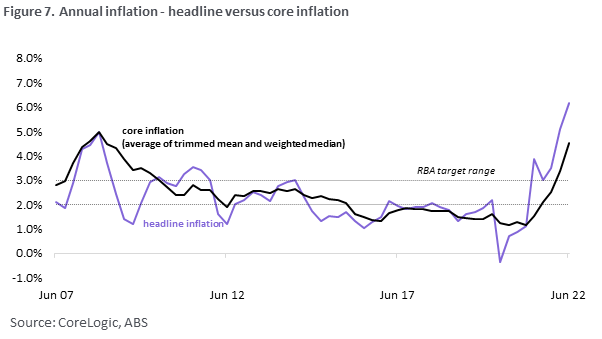

In the current climate, the most notable indirect impact of rising inflation on the housing market has been subsequent increases in the cash rate. This is because the RBA aims to influence inflation using the cash rate setting. The RBA targets a measure of core inflation, which strips out short-term, volatile influences on the CPI. Annual, core inflation is currently tracking at 4.5%, well above the RBA target range of 2-3%. Given that core inflation is unusually high, and the unique ‘emergency low’ cash rate settings through the pandemic, the RBA is now lifting the cash rate at the fastest pace since the 1990s.

As interest rates rise, and economic activity slows, inflation may be reduced. A consequence of this is that borrowing money to buy housing becomes less desirable, which in turn slows purchases and prices in the housing market. As CoreLogic has previously noted, this means there is an inverse relationship between the cash rate and changes in home values.

There is also some evidence to suggest that as home prices fall, household consumption could also go down – another indirect way higher interest rates help contain inflation. The RBA produced research in 2015 examining the relationship between increases in home values, and higher new vehicle registrations. The research concluded that there may be a more modest relationship between total household consumption and home values. Due to relatively high levels of household debt, most of which is housing debt, Australian consumption is likely to be more sensitive to increases in the cash rate, as mortgage costs increase.

Because of the strong relationship between home values and interest rates, inflation becomes a key indicator to watch when considering the outlook for the housing market. Once the RBA has an indication of inflation being contained between 2-3%, they will adjust cash rate settings accordingly.

So, how long will it take to curb inflation?

Inflation is expected to remain high in 2022, with a mix of domestic and international factors putting upward pressure on prices. Internationally, these include Russia’s invasion of Ukraine, the resurgence of COVID and COVID lockdowns in China, and capacity constraints in some segments of the economy. Domestically, extreme weather events have contributed to increases in some food items, and resilience in household spending remains an uncertainty.

However, there are early signs of relief in supply and demand pressures in the economy. In the US, a build-up in inventory is seeing retailers mark down the cost of some goods, while global input and commodity prices have also started to ease. Money markets are indicating a lower peak in the cash rate than originally anticipated a few months ago, and CBA has suggested RBA cash rate cuts could be in store as early as next year. If these trends in easing inflation begin to manifest more widely, it could signal a floor for the housing market decline as early as 2023.

Meet Eliza Owen

Head of Residential Research Australia

Eliza Owen was appointed the Head of Research at CoreLogic Australia in 2020.

Full profile