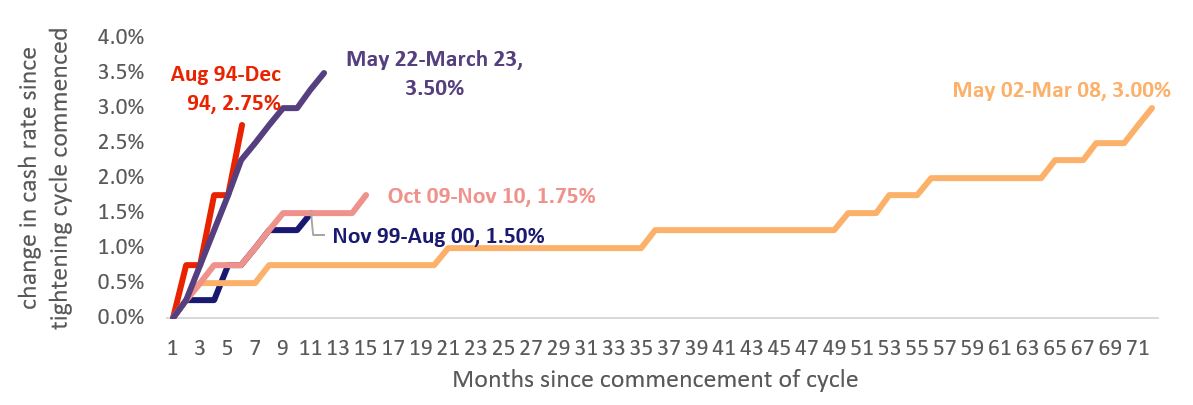

Today’s RBA decision for a 25 basis point lift takes the cash rate to 3.6%, the highest level since May 2012. To date, this rate tightening cycle has been both the largest and the most rapid on record by some margin.

The cash rate setting is now 105 basis points above the pre-COVID decade average (2.55%) and today’s hike adds roughly $160/month to repayments on a $500,000 variable rate owner occupier mortgage*. Since the rate hiking cycle commenced in May, mortgage repayments on a $500,000 home loan have increased by just over $1,000/month for owner-occupiers.

RBA rate tightening cycles since 1990

The decision to raise interest rates further was well telegraphed by the RBA after the February board meeting (and reiterated in the board meeting minutes), where the accompanying statement highlighted concerns inflationary pressure could become entrenched amid wages and price data exceeding the RBA’s expectations. Notably, after the February RBA board meeting, wage price data came in lower than market expectations, however this doesn’t seem to have swayed their resolve to push rates higher in an effort to quell inflation.

Since October 2021, lenders have assessed new borrowers on their ability to service a mortgage under an interest rate scenario that is at least 300 basis points above their origination rate. With the cash rate now 350 basis points higher through the hiking cycle to date, along with cost of living expenses probably well above what was budgeted, more households are likely to be facing balance sheets that have become thinly stretched.

Although 90+ day mortgage arrears were around record lows at the end of last year, it would be naïve to expect mortgage delinquencies to remain at such low levels. However, a trend towards improved underwriting standards, including lower proportions of high debt-to-income ratio lending and high loan-to-valuation ratio lending since early 2022, should help to keep mortgage defaults relatively low.

An expectation that labour markets will remain relatively tight is another factor that should also help to keep a lid on mortgage defaults. Forecasts from the RBA and Treasury, as well as the private sector, have the unemployment rate holding below 5% over the forecast period and well below the decade average of 5.5%. However, the higher interest rates go, the larger the risk that unemployment rates could rise above forecasted levels.

With interest rates moving higher, we are still seeing housing risks skewed to the downside. Arguably the full extent of the aggressive rate hiking cycle is yet to flow through to households. Variable mortgage rate adjustments take some time to impact existing borrowers, and there is also a larger than normal portion of mortgages on fixed terms that have been insulated from rate hikes to date. As the ‘bulge’ in fixed rate lending that occurred through 2020 and 2021 expires, more households will see their interest repayments adjust higher.

Since interest rates started to rise, CoreLogic’s combined capital cities Home Value Index is down 9.1%. Most housing forecasts have the peak to trough decline at around 15%. Although the rate of decline has flattened out over recent months, there remains a distinct possibility the housing downturn could reaccelerate due to the risks outlined above.

Meet Tim Lawless

Executive, Research Director, Asia-Pacific

Tim is executive research director of CoreLogic’s Asia–Pacific research division, managing a team of economic and data specialists across Australia and New Zealand. He brings more than 20 years’ experience to the role, providing deep insights and analysis on national housing trends.

Full profile